By Tim Toohey, Head of Macro and Strategy.

In our December 2024 economic outlook we noted:

“It is highly likely that the next four years will bring heightened volatility as markets return to being reactive to Trump’s predilection to make shock announcements.

“If Trump’s plan was implemented in full, we believe US inflation would be ~1% higher than the baseline scenario and US economic growth would be ~0.75% lower in 2025-26. The impacts are smaller if the US only impose tariffs on China, but there is no scenario in which an escalation in trade restrictions boosts economic growth and lowers inflation. If fully implemented, we believe Trump’s US$7.5 trillion in election promises will push government debt to economically unsustainable levels over the next decade.

“We believe that financial markets are underestimating Trump’s intentions.”

Liberation Day has just reinforced President Trump’s reputation as a shock agent. When faced with an array of choices, history tells us that his instinct is to choose the most extreme option on the table. After floating the idea that it was down to a choice between a universal tariff or country specific tariffs, financial markets actively positioned for a watered-down tariff policy announcement.

However, financial markets were again under estimating Trump’s intent and once again Trump took not only the extreme option, he took an option that was not even really on the table at all. Financial market surveys revealed that market participants were expecting the effective US tariff rate to rise no more than 12-15%. The results of today’s announcement are to raise the US effective tariff rate to 28% (before exclusions), essentially doubling market expectations and returning US tariffs to levels not seen since the first Model T Ford rolled off the production line in 1908.

Our initial calculations in December were based on 10% universal tariff and a 60% tariff on China (the policy Trump campaigned upon). Including wholesale and retail margin compression and substitution effects we arrived at an estimate of just over a 1% additional boost to US core inflation, pushing US core inflation to around 3.5% if fully implemented.

However, what was announced today was different. It certainly had the 10% universal tariff and an effective tariff on China that is 54% – close to the 60% Trump campaigned upon – however, it’s the bi-lateral tariffs on other nations that has really upped the ante for inflation.

On our calculations, we are now staring at a US core inflation impact that in the absence of a materially weaker US economy would take US core inflation to in excess of 4%. But here’s the rub. The US economy will be weaker. Much weaker than US economists are currently estimating. The impact of sharply reduced demand will take some of the heat out of inflation pressures, but not all of it.

So here is the basic math.

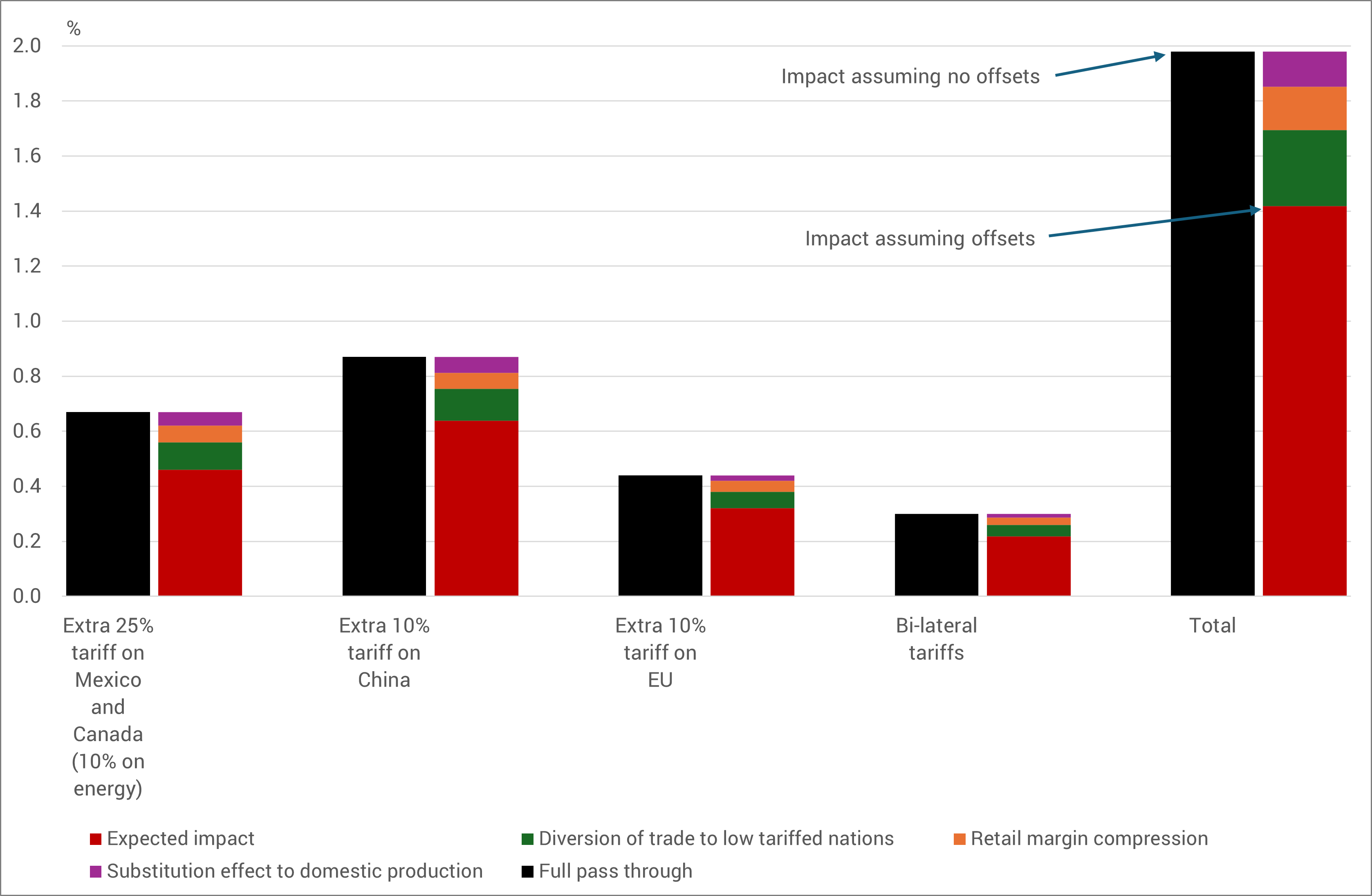

We have looked at a range of studies and the experience of Trump’s first term tariffs to gauge the size of any offsets from the full and permanent application of the various tariff rates to individual countries’ trade with the USA. These offsets include estimates of likely substitution to domestic US production, retail margin compression inside the US and diversion of trade impacts to other low tariff nations.

In Chart 1 below, we show both the full impact by selected region (black bars) and our estimate of the likely impact upon core PCE (red bars) once these offsets are accounted for. In short, we estimate that today’s announcement will add 1.4% to core PCE inflation in 2025-26. If nothing else changed, this would take the current rate of core PCE from 2.8% to 4.2%.

Chart 1 – Estimated impact of permanent tariff increases on core PCE inflation

Source: YarraCM.

However, this forecast is based on the assumption that everything else remains largely unchanged. But in reality, things can and inevitably will change:

- The first is that there could be a major escalation by retaliation from other nations, in particular Europe and China. This would not only lift the inflationary estimates shown in the chart materially higher, it also turns a largely US self-imposed tax into something that is truly global in nature. Under this scenario, non-US economic growth would also require a material downgrade and induce a secondary shock to the global economy.

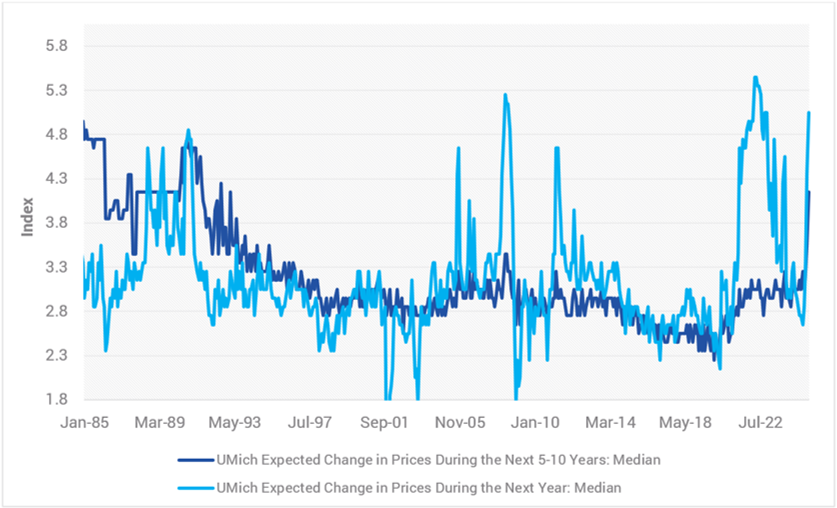

- The second is that inflation expectations become increasingly unanchored, turning the shock from a one-off price level effect to a persistent inflation problem that may require an interest rate response. Although Fed Governor Powell doesn’t want to acknowledge it, that cat may already be out of the bag (refer Chart 2). The Michigan Survey of Consumers has been screaming that message for two months now, but it is clear firms and forecasters have a lot to digest and soul searching to do in coming days. It seems impossible to conclude anything other than medium term price expectations are going higher and this hamstrings the Fed’s ability to react to the risks to economic activity and employment in a timely manner.

Chart 2 – Inflation expectations are skyrocketing

Source: University of Michigan, YarraCM.

- The third thing that can happen is that the announcement has simply such an adverse impact upon confidence – e.g. new orders from firms, investment plans and employment – that it causes an abrupt shock to economic activity.

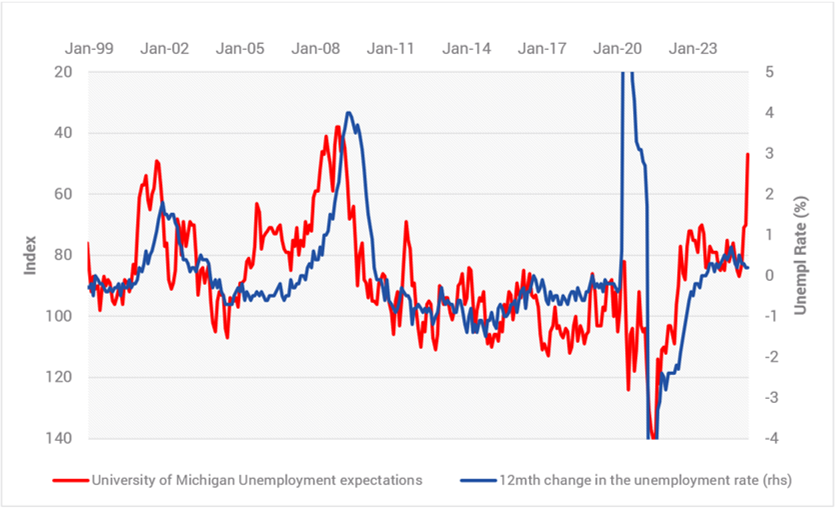

This also appeared well advanced ahead of today’s announcement and one can only assume the news flow sentiment from both consumers and businesses is going to lurch lower in coming days. If rising unemployment expectations (refer Chart 3) are matched with actual unemployment increases, it will be difficult to conclude that the US could avoid a recession in coming months.

President Trump may well learn that sometimes there are limits to his shock and awe approach.

Chart 3 – Unemployment expectations are following

Source: University of Michigan, YarraCM.

Stagflation is a word that financial markets love to throw around at will, when, in reality, it is a rare economic event requiring special initial conditions. Nevertheless, financial markets are going to be uttering that word ad nauseum in coming months as the real economy impacts unfold.

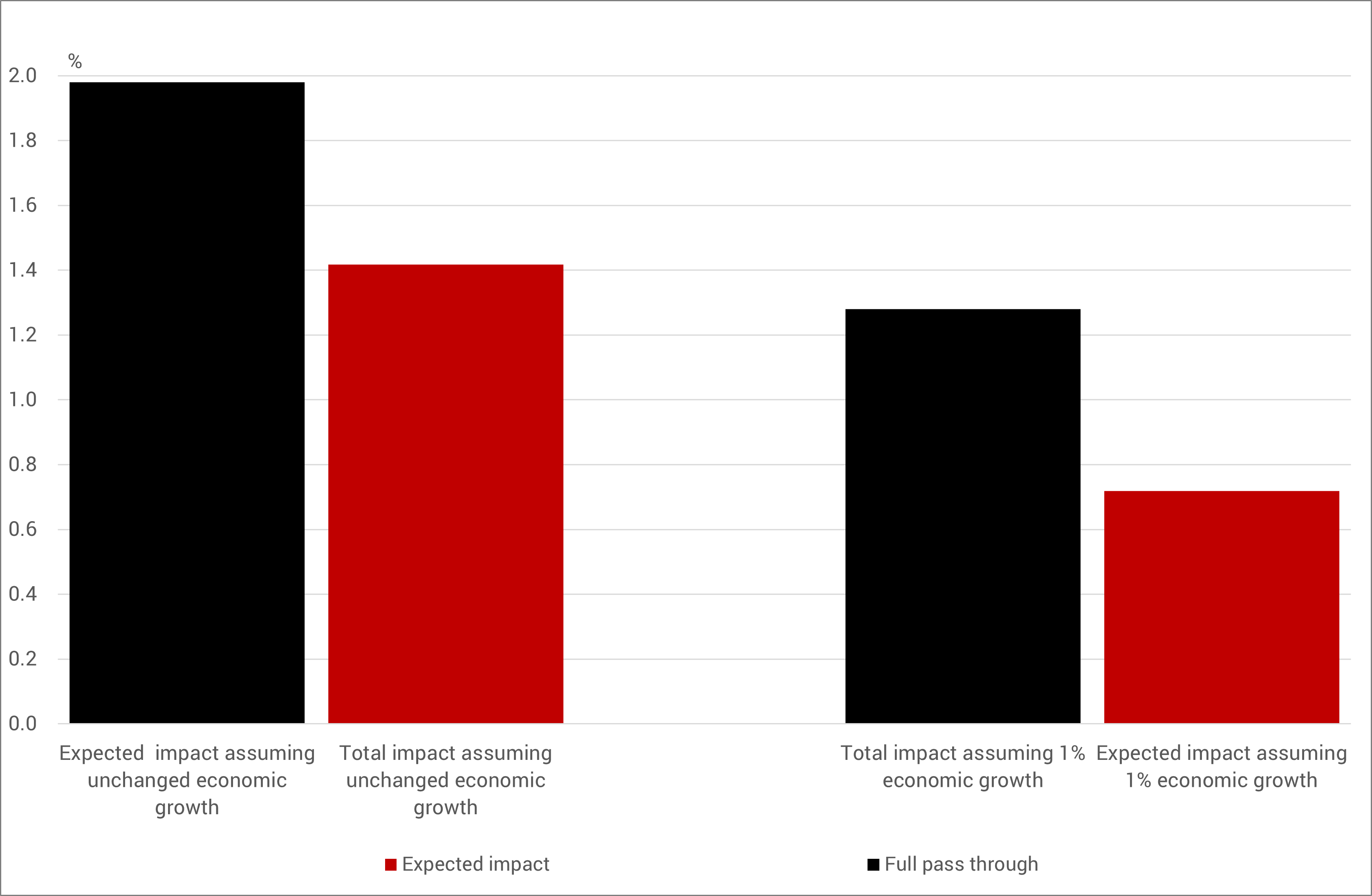

For our part, we revised down our US growth forecasts to 1.75% in 2025 and 1.25% in 2026 back in December 2024 fearing Trump would enact his election promises. Today he went further, and we are revising US economic growth to 1.0% in 2025 and leaving our 2026 forecast at 1.25%.

We are explicitly forecasting that weak US activity will force a severe bout of margin compression as firms are forced to clear inventory and weak sales growth translates through to weaker wages growth and rising unemployment.

Outside of a full recession scenario there are limits to this process and we estimate that the inflationary offset from a weaker US growth scenario reduces the inflationary impact from tariffs by ~0.7% in 2025-26 year, taking our estimate of the actual impact of the tariff policy from 1.4% to 0.7% (refer Chart 4).

Note this is still sufficient to take core inflation to 3.5% in 2025-26 and importantly this is assuming minimal retaliation from other countries. In other words, it could still be worse.

Chart 4 – Estimated impact of permanent tariff increases on core PCE inflation

Source: YarraCM.

To state the obvious, this is far from a good scenario for risk markets, especially given the starting point for 2025 of expensive markets embedding overly optimistic US economic growth and earnings estimates.

From a multi-asset perspective, we have been recommending a cautious approach to markets since late 2024 and we are currently materially overweight fixed income and cash, neutral credit and underweight equities and real assets.

We are awaiting material revisions to both US growth expectations, inflation and earnings together with any signs of a policy pivot by Trump or the Fed before shifting to a more risk friendly stance. Unfortunately, given Trump’s stubborn belief and the Fed’s focus on inflation expectations it is likely to take an uncomfortable amount of time before someone blinks.

For the RBA, our view has been that they will cut in May and again in August 2025 before re-engaging in 2026 with additional easing. However, the events of today give greater impetus for the RBA to act – Trump’s policies present a clear attack on our region and our major export nations.

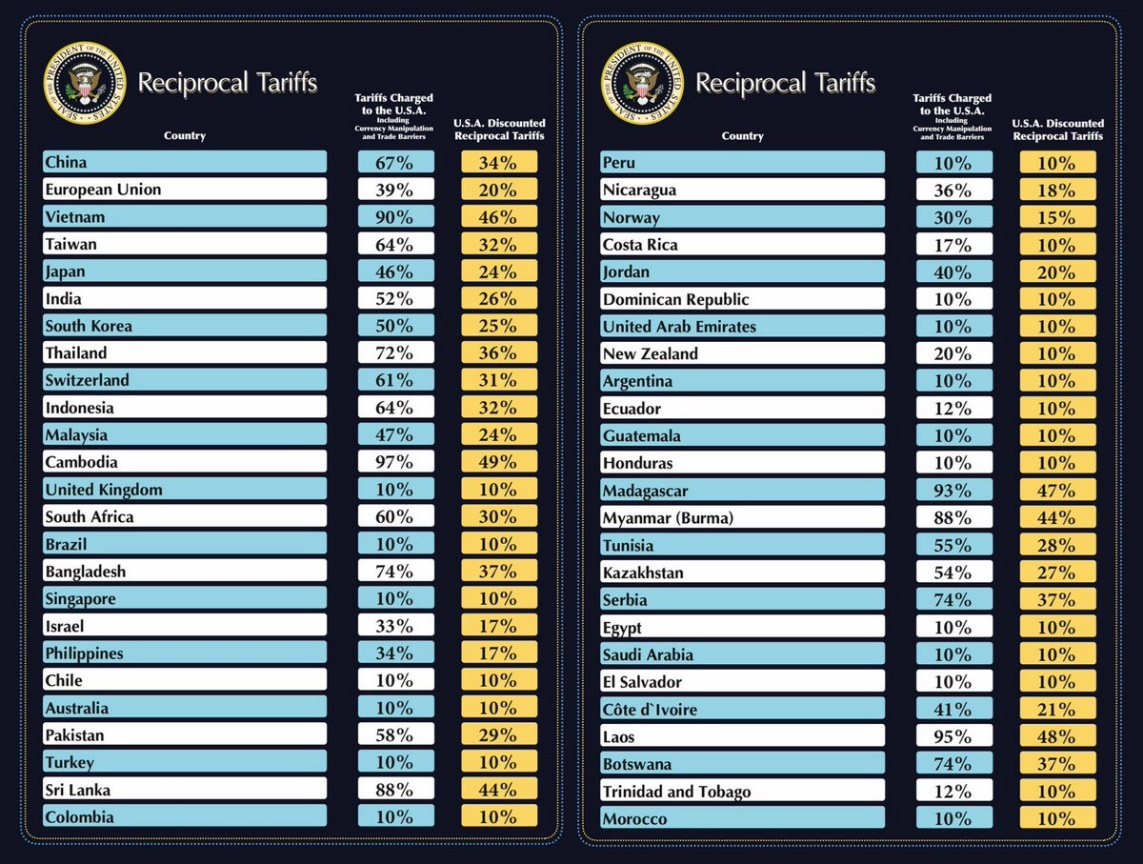

Figure 1 – US Government’s Tariff Agenda

Source: YarraCM.

It is notable that the tariffs on much of Central and South America are set at or close to 10% but Australia’s near neighbours and significant trading partners are being targeted far more aggressively. There is a clear bias to punish China and countries in which China has large surrogate manufacturing bases. Vietnam, Taiwan, Thailand, Cambodia, Bangladesh and Sri Lanka have all been slated with tariff increases in the mid-30% range for additional tariffs. For each of these countries the US is between 18-30% of their exports and the #1 export market.

From Australia’s perspective we are likely to see Asian export trade diverted from the US to our shores, so we can expect cheaper clothing, textiles, computer and telco equipment, steel and auto parts to flood our shores in coming months. However, this will represent massive competitive threats to local manufactures in these industries.

It was notable that Taiwan received a hefty 34% increase and Japan copped a 24% tariff hike. Australia exports A$37bn in coal and $30bn in gas to these two nations. Including China, which is now facing a 54% tariff and where we send a further $30bn in coal and gas and a massive $116bn in iron ore, the risks to our export markets are clear. If economies in the Asia region cannot find a way to stimulate sufficient domestic demand in a short timeframe, then Asia will clearly bear a disproportionate impact from Trump’s trade announcements.

As a result, we are adding additional easing in our forecasts and now expect the RBA to ease in May, August, September and November. If the RBA were uncertain on Tuesday, then their heads must surely be spinning today.

0 Comments